Getting Ready To Trade Notes

I previously wrote about my experience with Lending Club. None of my loans have turned rickety and I have even signed up for FOLIOfn’s Note Trading Platform. Here is what Lending Club has to say about trading:

If you are a Lending Club lender and wish to sell some of your Notes, or buy Notes currently held by other lenders, you can now use the Note Trading Platform operated by FOLIOfn, member FINRA/SIPC. You will need to open an account with FOLIOfn, but you can use the funds available in your Lending Club account to buy Notes through the Trading Platform, and receive the proceeds of any sale of Notes (minus a 1% trading fee) directly into your Lending Club account. Only Notes that were issued after October 12, 2008 can be traded on the Trading Platform.

Just when I was getting used to doing business with Lending Club, I now have to work with FOLIOfn. This is what Wikipedia says about this company:

FOLIOfn, Inc. is a brokerage and investment company serving investors, financial advisors, and financial institutions around the world. FOLIOfn offers its brokerage services on both a full-service basis and a technology-licensed basis. Through its wholly owned, registered clearing broker-dealer subsidiary, FOLIOfn Investments, Inc., the company offers an integrated brokerage and technology platform featuring its patented Folio trading capability, as well as execution, clearance and settlement services. The company also operates Proxy Governance, Inc., which provides corporate governance-related services to companies. Steven Wallman, a former commissioner of the Securities and Exchange Commission, established the company in 1998. The privately held company is headquartered in Vienna, Virginia.

Trading Advantages

It was straight-forward enough to sign up and now I am ready to buy a Note. As a trader I can review loan payment history and credit score changes since the date the loan was issued, as well as the original loan listing. However, the listings are not updated to reflect changes in the credit worthiness of the borrower. I can buy Notes that have a shorter time period to maturity. I may be able to find Notes priced below their fair value. And it is the seller that pays the 1% trading fee.

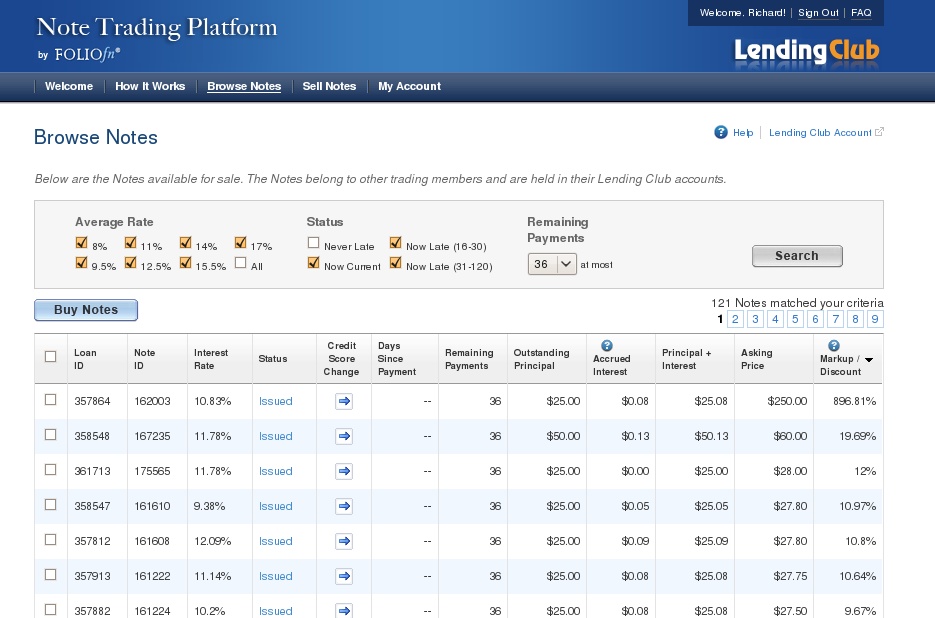

Finding Notes To Buy

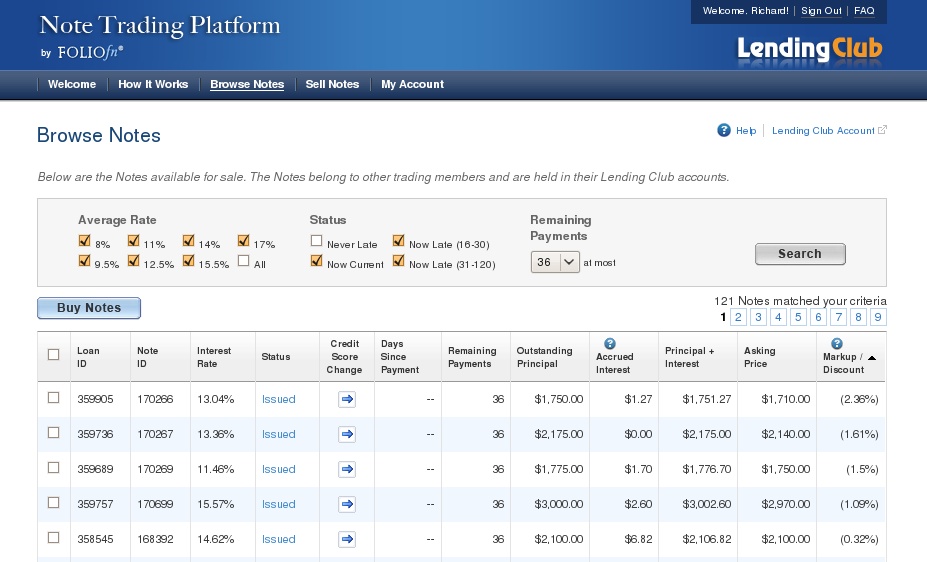

I click on “Browse Notes” and take the default search settings. 121 Notes match my criteria and I sort on “Markup/Discount”. This is the difference between the Asking Price and the sum of Outstanding Principal and Accrued Interest. The highest markup is 896.81% on a $25 Note. I think the Asking Price of $250 had a zero accidentally added. There are 93 more Notes with markups between 2.71% and 19.69%. I’m looking for a discount so I sort on “Markup/Discount” again. This doesn’t look too promising either. Anything with the slightest discount is $500 or more and the highest discount is 2.36% if you are willing to invest $1,710. Over time these discounts will rise and you will be able to pick up some bargains. They have already improved since the last time I looked.

{kind=link}

{kind=link}

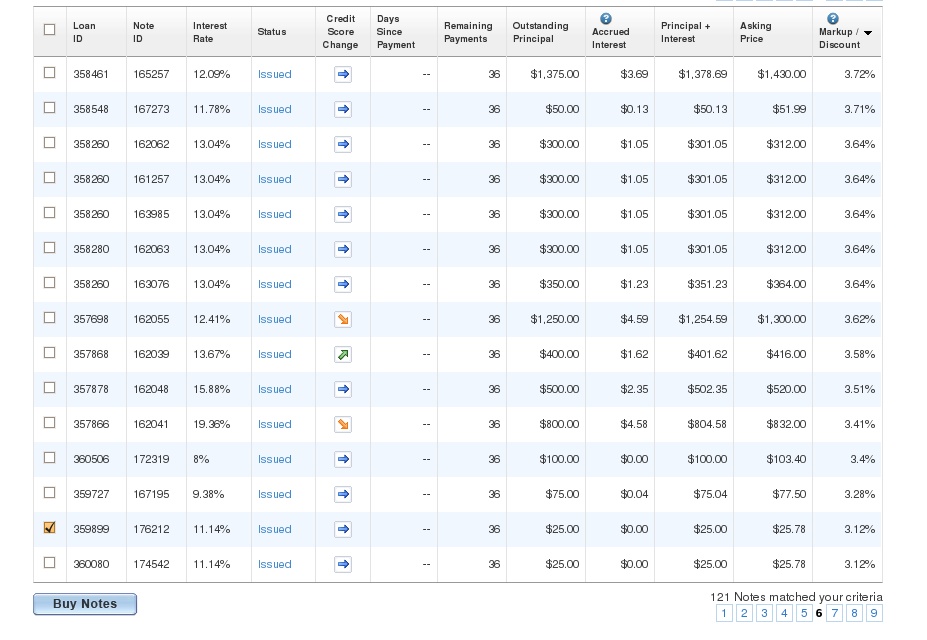

Buying A Note

In the meantime I will buy a $25 Note to finish the process. Notice in this snapshot that I pay a markup of 3.12% or 78 cents. Some of the loans on this page have had a Credit Score Change that is indicated by the direction of the arrows. This is a very handy chart with a lot of information and a link back to the original loan. My purchase goes through and I get the message:

{kind=link}

We have received your order to buy 1 Note for a total purchase price of $25.78. Your order will settle today if we received your order before 11am Pacific time on a business day. Otherwise your order will settle on the next business day.

It is that simple. Of course you wouldn’t normally take a loss of 78 cents but I wanted run through a buy to the conclusion.

Information About Notes

Each listing contains the Note’s interest rate, issue date, outstanding principal, accrued interest, number of payments left, and payment history to date. The Notes are not re-graded over time but variations of the credit score of the underlying borrower since the issue date are shown.

Accrued Interest

The Notes traded through the Trading Platform pay monthly interest. The payment date varies with each Note. The buyers receive interest payments, irrespective of whether they buy the Note on the first day after the previous payment has been made, on the last day before a payment is being made, or any time in between. Accrued interest since the last payment date is displayed on the Browse Notes page.

Summary

I have not sold any Notes yet but it should be as simple a process as buying. I anticipate much better deals on the Notes for sale in the near future. Notes with only one or two years left to maturity should be more appealing. I really like the idea that I can liquidate my loans if I need cash. Eventually I think that there will be many peer to peer lending websites. With Lending Club’s low default rate they are helping to blaze the trail for the do-it-yourself bankers like me and you.

There is another p2p site on its way to launch soon. It is http://www.yadyap.com (payday backwards). The platform is specific for peer-to-peer payday loans. The goal is the create better rates for people that typically get stuck in the payday loan trap, while at the same time delivering good returns to lenders.

Thank you for the information, I was not aware of your site. It looks like the loans will be for 2 to 4 weeks and allocated by auction. I will be sure to check it out. I have several friends that are following my adventures on Prosper and Lending Club. With your very short loan life it should be easy to test it out and see what kind of returns are possible, all within a few months or even weeks. I wish your company well.

Yours is an interesting website. I would think that funding an entrepreneur is no more risky than loaning money to fund a credit card consolidation loan. However, I’m not about to try it any time soon. With all P2P lenders on notice that they have to register with SEC I am a little gun-shy of all these companies. Loanio that just launched last month, has suspended new loans until it registers with the SEC. Lending Club is already registered.

Thanks for the great info. I really think that with all that’s going on in the banking world these days, P2P can gain a strong foothold…if the federal regulations/requirements get sorted out.

Jum,

P2P looks like it will take off, I agree. If the big banks were smart they would be working on their own P2P companies.

Hi Rickety,

First time on your site. This service looks very interesting. I never imagined that a web site that featured Peer 2 Peer buying and selling notes notes would even exists. I will sure take a look at Foliofn to see if I can participate. I live in PR so I cannot participate in most online investing sites but I will surely take a look. Thanks for the valuable info.

Spark,

It looks like you can’t participate. Check out this Lending Club blog entry.

Trading loan is good since you can keep track with your loan payment history. It provides service that will surely respond to the need on investors or buyer of notes. Nowadays various scheme of granting loans are made convenient to the customers such as the payday loans online. It is pretty convenient for people that need them. A lot of people are very busy, or have schedules that don’t allow them to be able to get to an actual store before closing time, which is why payday loans online would be good for them. It’s an easy process, and it is guaranteed to be safe and secure, as most lenders have stringent safety and security measures. All you need is the standard things, like a bank statement of an open and active checking account and proof of employment.

It looks like this new company that you’re trading through isn’t so bad. It’s just going to take time to get used to it. I hate change too. Doing this sounds interesting and I’m glad I came across this post and had a chance to learn from your experiences.

I ended up liquidating all my loans and breaking even. However, I have a family member who is doing well with his loans. I may get back in at a later date.

First of all I would like to say how nice it is that you take the time to respond to comments. I’m glad you at least broke even. It still sounds promising. If you get started again, I hope you post about it and keep us updated.

I was planning on posting some tips from a family member who is an active lender. I just need his permission.

Peer to peer lending is the way to go. As long as people try not to give the system a bad reputation by defaulting on loans(as some have), it will continue to grow in popularity.

I thinks this is related to Forex Trading. Anyway, thanks for sharing.